Moving Tips

Comprehensive Guide to Moving Insurance: Coverage, Costs, & Tips

Moving to a new home is exciting, but it also comes with risks. When you hire movers, your belongings will be packed, transported, and unpacked by strangers, which might leave you feeling apprehensive. This is where moving insurance coverage comes in. Moving insurance provides financial protection for your possessions in case they get lost or damaged during the move. There are always pros and cons to hiring professional movers—even with a top-notch moving company, accidents or unexpected events like bad weather or road accidents can happen. Having the right insurance coverage ensures you won’t be left footing the bill if something goes wrong, giving you peace of mind and a truly stress-free move.

What Is Moving Company Insurance?

Moving company insurance coverage refers to the liability protection and insurance options that cover your household goods during a move. In the U.S., licensed interstate movers are required by federal law to offer two levels of liability coverage for your shipment. These levels are often called "valuation coverage" and come in two forms: Released Value Protection and Full Value Protection. Essentially, this is the mover’s promise to compensate you up to a certain amount if your items are lost, damaged, or destroyed while in their care. It’s important to understand that the moving company's coverage is not automatically all-encompassing—you need to choose the level of protection that matches your needs. In addition to the mover’s own coverage, you also have the option to buy separate third-party moving insurance for extra protection.

In short, moving insurance coverage is crucial because it holds the moving company accountable for your goods and can reimburse you if mishaps occur, ensuring you’re not left with losses. If you're still wondering why this coverage is so important, imagine expensive electronics, heirlooms, or all your furniture getting damaged in transit. Without proper coverage, you’d have to replace those items out-of-pocket. With moving insurance, however, you are financially protected. It’s a safety net that makes a stress-free move possible, giving you recourse (and funds) to repair or replace your belongings should the unexpected happen.

Types of Moving Insurance Coverage

When planning a move, it’s essential to know the different types of moving insurance coverage available. In the United States, there are three primary coverage options to consider.

Released Value Protection (Basic Coverage)

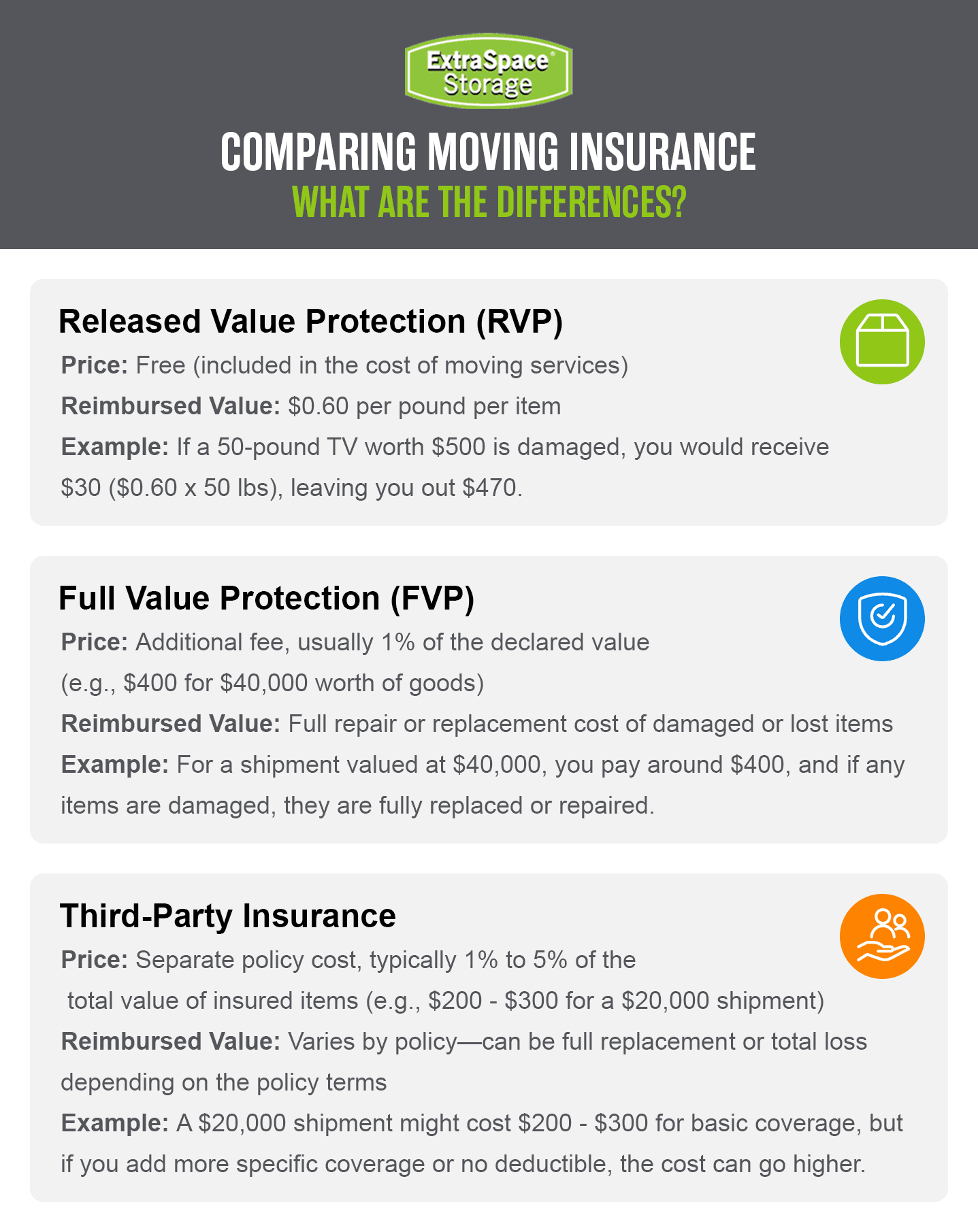

This is the most basic coverage your moving company offers, and it’s included at no extra cost. Under Released Value Protection, the mover’s liability is minimal—only up to $0.60 per pound, per item, mean you'd be reimbursed by weight rather than actual value. For example, if a mover drops your ten-pound lamp that’s worth $300, you’d get at most $6.00 ($0.60 x ten pounds) as compensation. Clearly, this basic moving company insurance coverage does not provide full replacement value for most items. It’s essentially a token amount mandated by law as the default coverage. Because it’s so limited, you must sign a waiver on your bill of lading if you choose Released Value, acknowledging that you agree to this lower level of protection. Released Value Protection is best for those willing to accept minimal reimbursement—perhaps if you have mostly low-value, replaceable items or you’re moving on a tight budget. Just remember that if something happens, this coverage won’t come close to covering the actual value of high-priced belongings.

Full Value Protection (Full Replacement Coverage)

Full Value Protection is a much more comprehensive coverage option. If you select this coverage, the moving company is liable for repairing, replacing, or reimbursing you for the current market value of any item that is lost or damaged during the move. In other words, under Full Value Protection (FVP), if your $500 tablet gets damaged, the mover must either fix the item, replace it with a similar one, or pay you its fair market value (depreciation is typically considered, so you’d get the value of a used item, not brand-new). This coverage must be purchased—it’s not free like Released Value. Often, the cost is based on the total value you declare for your goods. For instance, a common rule of thumb is around 1% of the declared value of your shipment. If you estimate your belongings are worth $50,000, full protection might cost roughly $500. However, every mover’s pricing can differ, and some may offer tiers or deductibles to adjust the cost. With FVP, movers can also set terms. For example, they may have a minimum declared value (such as a formula based on $5 or $6 per pound of your shipment weight) and may require you to list high-value items—typically those worth over $100 per pound—in writing to ensure full coverage. Full Value Protection provides more peace of mind, especially if you have high-value items, as it requires the mover to compensate you for any covered loss or damage. In fact, federal regulations make this the default coverage on interstate moves unless you waive it—meaning if you don’t explicitly choose Released Value, your shipment will automatically be at Full Value Protection level (and you’ll be charged for it). While FVP costs more, it provides significantly better coverage, making it worth considering if you want maximum protection.

Third-Party Moving Insurance

In addition to the mover’s own coverage options, you can purchase separate moving insurance from a third-party insurance provider. These policies are offered by independent insurance companies and can supplement or extend coverage beyond the mover’s liability. Third-party insurance can be useful if you have valuable or fragile items that the standard coverage won’t adequately protect. Typically, if you buy third-party moving insurance, the moving company’s basic liability (e.g., the $0.60 per pound from Released Value) still applies first, and then the insurance policy will cover the remaining loss up to the policy limit. For example, if your TV is destroyed and it weighs 30 pounds, the mover would owe you $18 under Released Value, but your third-party policy could pay the difference up to the full value of the TV. Third-party policies often cover risks that mover coverage might not, such as catastrophic events—like a truck accident, fire, flood, or theft—that could result in total loss. The cost for third-party moving insurance can range from about 1% to 5% of the value of your goods, depending on the level of coverage and deductible you choose. You can get this type of insurance through a company that specializes in moving insurance, or even through your homeowner’s insurance provider as a rider. It’s important to read the terms—some third-party policies only cover total loss (i.e., the entire shipment destroyed), while others can cover damage to individual items. Use third-party insurance if you have especially high-value belongings—like fine art, antiques, and jewelry—or if you simply want additional peace of mind beyond what the moving company offers. Before purchasing, review the policy terms to avoid any surprises later—and always keep a copy for your records.

How to Choose the Right Moving Insurance Coverage

Choosing the best insurance coverage for your move depends on your individual needs, the value of your belongings, and your budget. By considering these factors, you can confidently choose moving insurance coverage that leaves you feeling confident and supported during your move. Here are some tips and considerations to help you select the right coverage.

Assess the Value of Your Belongings

Start by taking inventory of what you plan to move. Do you have a lot of high-value items—expensive electronics, antique or curated furniture, heirlooms, artwork, etc.? If your possessions include items that are costly or irreplaceable, the basic $0.60-per-pound coverage will likely be far from sufficient. On the other hand, if you’re moving mostly clothes, books, and inexpensive furniture, you might be comfortable with minimal coverage. Be honest with yourself about the level of risk you’re willing to accept.

Consider the Distance & Risk Factors of Your Move

Are you moving just across town or across the country? Long-distance and cross-country moves involve more miles on the road, which inherently increases risk of accidents or damage. Consider external factors and what time of year you're moving, as well—for example, moving during hurricane season or in winter can introduce weather-related risks. If you know your route or timing could expose your goods to greater risk—rainy weather, rough roads, high traffic accident areas, etc.—it may be wise to opt for a higher level of coverage. Local moves generally have less risk, but damage can still happen even on short trips.

Check Your Existing Insurance Policies

Before buying additional moving insurance, see what coverage you might already have. Sometimes, homeowners or renters insurance provides limited coverage for personal property during a move, but often it’s very restricted or requires a special endorsement. Don’t assume you’re covered—many homeowners/renters policies offer limited coverage or do not cover goods in transit at all. Call your insurance agent and ask specifically about coverage for items during a move. If your current policy does offer some protection, find out the limits and deductibles. You might still need extra moving insurance, but you can at least avoid paying for duplicate coverage. If you’re moving items into storage, you can also check to see if your insurance covers that or if you need separate storage insurance.

Compare the Coverage Options Offered

When you get a quote from a moving company, they should explain the insurance/valuation options available. Ask for the price of Full Value Protection for your shipment value, and what it would cover. Also ask for examples of what their basic coverage really means in dollars. Some movers might have different deductible levels for full protection (e.g., you pay a lower premium if you agree to a $500 deductible on any claim). Get those details and costs in writing. Then, weigh the cost vs. the risk. As a rule of thumb, full protection might add roughly 1% (or a few hundred dollars) to your moving cost, depending on the moving company and coverage terms. For most people with any significant furniture, electronics, or other valuables, this cost is often worth it for the peace of mind it provides. If the mover does not offer a full value option—which is unlikely for interstate moves, since it’s required—or if their coverage seems insufficient, that’s a red flag. Consider a different mover or look into third-party insurance.

Consider Third-Party Insurance for Special Situations

If you have extremely valuable items that exceed your mover’s coverage limits, or if you’re particularly worried about things like fire, theft, or breakage of fragile collections, look into third-party moving insurance. This can be in addition to the mover’s Full Value coverage for an extra layer of protection. For example, if you have a grand piano or a piece of fine art, a specialized insurance policy might cover it for its appraised value in the event of significant damage or loss. When choosing a third-party policy, compare providers and read reviews—some insurers specialize in moving and relocation insurance. Also, make sure you understand how to file a claim with that insurer in conjunction with the mover’s process. The cost will be higher for higher coverage limits, so you'll need to decide if only certain high-value pieces need extra coverage or if you want a policy covering everything

Read the Fine Print & Ask Questions

Before finalizing your decision, ask the moving company about anything you’re unsure of. For instance, are there any exclusions with the coverage? What is the process if you have to make a claim? Do they require proof of value for expensive items? Reputable movers will provide a brochure or document—like the federally mandated "Your Rights and Responsibilities When You Move" booklet—that outlines your insurance options and claim procedures. Take time to read it. Being informed will help you choose wisely. If something isn’t clear, don’t hesitate to get clarification. It’s better to know exactly what coverage you have than to get an unpleasant surprise later. Remember, the goal is to match the coverage to your specific move, so choose a plan that leaves you feeling secure and financially protected.

Costs, Benefits, & Limitations of Moving Insurance

When budgeting for your move, it’s important to factor in the cost of moving insurance and weigh it against the benefits it provides. Let’s break down the pricing, advantages, and limitations of moving insurance.

Cost of Moving Insurance Coverage

The price you’ll pay for moving insurance depends on the type and amount of coverage you select. Here’s a general overview:

Released Value Protection: Free. This basic coverage is included in the moving services by law, so it doesn’t add anything to your bill. However, it’s "free" for a reason—the coverage level is very low (only up to $0.60 per pound per item). So while you won’t pay extra for RVP, you’ll want to understand the potential cost to you if something breaks. For example, if a 50-pound TV worth $500 is destroyed and you only have RVP, the mover pays you $30 ($0.60 x 50 pounds). You’d be personally out $470 to replace that TV. In essence, the true cost of opting for minimal coverage could be the replacement money coming out of your own pocket in case of damage.

Full Value Protection: Additional fee based on your declared value. Full Value Protection usually costs extra, typically calculated as a percentage of the total value of the shipment. Many moving companies charge around 1% of the declared value, though costs can vary. Using that rule of thumb, if you declare your household goods are worth $40,000, full protection might cost roughly $400. Some movers have set packages (e.g., $X for up to $Y coverage) or may let you choose a deductible to lower the premium. For instance, you might pay a bit less if you agree to a $250 or $500 deductible (meaning you cover the first $250/$500 of any claim). Always ask how the mover calculates full-value coverage cost. Also, be aware that if you undervalue your goods to save on the premium, you could be underinsured come claim time—so be realistic in your declared value. While FVP adds to your moving expenses, it covers the full repair or replacement value of items, which can potentially save you thousands of dollars if something goes wrong during your move.

Third-Party Insurance: Separate policy cost, varies by provider. If you opt for a third-party moving insurance policy, costs can range widely. On average, expect anywhere from 1% up to 5% of the total value of the insured items. The percentage will depend on the level of coverage (full replacement vs. total loss only), the deductible you choose (if any), and any special riders for high-value pieces. For example, insuring a $20,000 shipment might cost around $200 - $300 for a standard policy, but if you want coverage for breakage of individual fragile items or no deductible, it might be on the higher end of the range. Third-party insurance is an optional expense—it makes sense mostly if you need coverage beyond what your moving company provides. You might decide to get it only for particularly expensive items, as some insurers let you insure select items. Keep in mind, this cost is paid to the insurance company, not the mover. If you do buy a policy, include it in your moving budget and verify whether the policy requires any documentation (like an inventory or appraisal of high-value goods) to be valid.

Benefits of Moving Insurance

Here are the key pros to investing in moving insurance:

Financial Protection for Your Belongings: The primary benefit is that you won’t face the full financial burden if your items are damaged or lost during the move. With adequate insurance, you can get reimbursed for repairs or replacements instead of paying entirely out-of-pocket. This protection can be a lifesaver if an expensive item breaks or an entire shipment is affected by an accident.

Peace of Mind & Reduced Stress: Knowing your valuables are insured allows you to approach moving day with much less anxiety. You can focus on the excitement of settling into your new home rather than worrying about every "what if" scenario. Essentially, insurance buys you peace of mind. Many people find that this reduced stress alone is worth the cost—it lets you sleep at night during a move, confident that even if an accident happens, you’re covered.

Complete Coverage Options: With moving insurance, especially Full Value or third-party coverage, you have comprehensive protection for a wide range of incidents. From the minor (e.g., a scratched coffee table) to the major (e.g., the moving truck gets in a wreck), a good insurance plan can cover damages, loss, or even theft. By choosing the right level of coverage, you can make sure even your high-value items are properly protected. This flexibility means you can tailor the insurance to your needs—instead of being stuck with a one-size-fits-all option, you can decide how much risk you want to cover.

Quick Recovery & Continuity: When something goes wrong and you have insurance, the recovery process is simpler. You file a claim and get compensation (assuming all goes well), which means you can replace essential items and get your life back on track faster. Without insurance, you might have to wait or save up to replace things, which can disrupt your life. In this way, insurance provides a safety net that keeps your relocation on a positive track even if there’s a hiccup.

Required by Some Situations: In certain cases, having moving insurance (beyond the basic) might be effectively required. For instance, if you’re moving into a high-rise or a building that asks for proof of insurance from the movers, opting for full coverage may be part of meeting those requirements, since the building wants assurance that any damage in transit is covered. Additionally, if you’re moving for work and using a professional relocation service, they often insist you have adequate coverage for your shipment as part of the relocation agreement. While this isn’t a benefit in the traditional sense, it’s an important consideration that can make moving insurance a necessary part of the process.

Common Exclusions & Limitations

It’s equally important to know what moving insurance does not cover. No insurance policy is all-inclusive, and moving company liability has specific limits. Here are some typical exclusions or limitations to be aware of.

Owner-Packed Boxes (Internal Damage): If you pack your own boxes and something inside gets broken, the mover might deny liability unless the box itself shows obvious damage. For example, if you packed a box of dishes and they arrive shattered but the box looks fine externally, the mover’s insurance could claim improper packing on your part. Movers generally aren’t responsible for damage to contents of boxes they didn’t pack, unless there’s clear negligence (such as a box being crushed). This limitation means if you’re opting for full coverage, you might want to let the movers pack fragile or valuable items for you—or at least follow proper packing guidelines.

Natural Disaster: Most moving company coverage does not cover damage due to unforeseen natural events beyond their control (often termed "Acts of God"). For instance, if a sudden flood, wildfire, or hurricane destroys the moving truck and your belongings, the moving company might not be liable under Released or Full Value protections. These events are usually excluded from carrier liability. However, a third-party insurance policy might cover such disasters. Always check—if you’re moving through tornado country or during peak storm season, consider insurance that includes these scenarios.

High-Value Items Not Declared: As mentioned earlier, under Full Value Protection, movers can limit their liability for very expensive items if you don’t declare them in advance. Typically, anything worth over $100 per pound must be listed on the shipping documents—this is sometimes called the "extraordinary value" declaration. If you fail to list your $5,000 jewelry set or a rare collectible and it’s lost, the mover might only pay the default per-pound rate or deny full compensation. This isn’t exactly an exclusion—you can still get coverage for these items if you declare them—but it’s a common reason people mistakenly believe their insurance didn’t cover an item.

Certain Valuable Items: Some items—like cash, jewelry, and personal documents—may not be covered by moving company liability at all, often due to company policies or insurance restrictions. Movers usually advise you to carry cash, important papers, photographs, jewelry, and other small valuables with you, rather than putting them on the truck. In fact, many movers will not transport extremely valuable small items (or will do so only if you sign a waiver) because they don’t want the liability. As a rule, plan to keep these kinds of belongings with you in your personal vehicle or ship them via a specialty service with insurance. Similarly, sentimental items (like family heirlooms or one-of-a-kind keepsakes) have value beyond money—no insurance can truly compensate their loss, and movers know this, which is why they caution against putting them on the truck.

Perishables, Hazardous Materials, & Other Non-Allowable Items: If you pack items that movers prohibit (e.g., perishable food, plants, chemicals, or flammable items) and they get damaged or cause damage, insurance won’t cover it because those items shouldn’t have been on the truck to begin with. Always ask your mover for the list of "non-allowable" items they won’t move or that void liability. For instance, if you pack a bottle of bleach and it leaks all over your furniture, the damage might not be covered due to you shipping a prohibited item.

Storage Situations: If your goods will be stored before delivery or after pick-up as part of your move, clarify how insurance works in that scenario. If your items are in the mover’s storage facility, their liability should continue. But if you arrange separate storage or your items sit in a self storage unit for a while, the moving company’s coverage typically ends upon delivery to that storage. You’d then need separate insurance for the storage period. Additionally, if you’re doing a long-distance move with a van line and your items are transferred or stored in a trailer for a few days, make sure this is covered under your plan. Most full protection covers door-to-door, including short-term storage-in-transit, but it’s good to confirm.

Find Affordable Self Storage Near You

Extra Space Storage has over 4,000 locations across the U.S. with friendly customer service, advanced security features, and affordable month-to-month rates.

- Save up to 50% off online

How to File a Moving Insurance Claim

Nobody wants to imagine their belongings getting damaged or lost during a move—but if it does happen, you’ll need to know how to navigate the claims process. Filing a moving insurance claim involves a few important steps and deadlines. Here’s a step-by-step guide to help you handle the process efficiently.

Inspect Items Upon Delivery & Document Any Issues

When the moving truck arrives at your new home, don’t rush the unloading process. As each box or item comes off the truck, check it over, and have your inventory list in hand to tick off items. If you notice any damage or missing items, note it on the delivery receipt or inventory sheet before signing anything. If a box is crushed or a piece of furniture is scratched, point it out to the driver and make sure it’s recorded in writing. This documentation at delivery is crucial evidence for any claim. Additionally, take photos of the damage immediately if you can—photos provide clear proof of the condition of items when they arrived. If something is missing, note which item on the inventory wasn’t delivered. It’s best to unpack essentials right away and check for damage, but you may not be able to unpack everything on the spot. Make sure you at least inspect for any obvious problems and do not sign the final paperwork stating you received everything in good condition until you’ve done this initial inspection. (If the driver pressures you, remember you have the right to take the time you need for this.) By documenting issues at delivery, you establish a record that the damage or loss likely occurred during transit, not after.

Promptly Notify the Moving Company & Start the Claims Process

As soon as you discover any loss or damage, you need to initiate a claim with the mover. For interstate moves, you have up to nine months from the date of delivery to file a written claim, but it’s best not to wait that long. In fact, try to file the claim as soon as possible—timely reporting can make the process smoother and help you receive compensation faster. Contact the moving company’s customer service or claims department and inform them that you will be filing a claim. They will usually provide a claim form or direct you to an online claims portal. Follow their procedures carefully and make sure to keep a copy of everything you submit (including forms, emails, photos, etc.) for your records. Here are a few tips for the claim itself:

Put It in Writing: Regardless if you do so verbally, claims must be in writing (or electronic) to be valid. Fill out the official claim form or submit a written letter/email that clearly states it is a claim for loss or damage.

Identify Your Shipment: Include your moving contract number or bill of lading number, the pickup and delivery dates, and origin/destination addresses—basically, any info that helps the company locate your order in their system.

Detail the Items & the Damage: List each item you are creating a claim for, describe the damage (or note if it’s missing entirely), and state the estimated value or repair cost. Be specific—e.g., "Dining table: legs broken off, cannot be used. Replacement cost approximately $800." If you have receipts or appraisals for valuable items, include copies.

Assert the Mover’s Liability: In the claim statement, you can say that you are holding the moving company responsible for the loss/damage and requesting compensation under the terms of the coverage you purchased (Released or Full Value, or additional insurance). This makes it clear you expect them to pay.

Include Supporting Evidence: Attach the photos you took of the damage, and a copy of the inventory sheet where the damage was noted at delivery. The more documentation included, the stronger your claim.

Cooperate with Any Inspection or Follow-Up

After you file, the moving company might assign a claims adjuster or ask for additional information. In some cases, they may send an inspector to look at the damaged items in person or request you get a repair estimate from a shop. Be responsive to these requests and keep notes of all communications. If an item is repairable, the mover might choose to have it repaired instead of paying full replacement—which is their right under full protection coverage. You might be asked to get a quote for repair costs—if so, send it to the mover. Always communicate in writing (email works well for creating a paper trail) and save all claims-related messages.

Know the Timeline & Your Rights While Waiting for Resolution

By law, for interstate moves, a moving company must acknowledge receipt of your claim within 30 days of receiving it and must provide a final response (offer of settlement or denial of claim) within 120 days. Should they need more time for any reason, they're expected to notify you with a clear explanation and resolve the matter promptly. Mark these key dates on your calendar—if 30 days pass unacknowledged, politely follow up and reference the requirement. During this time, do not dispose of any damaged items unless the mover tells you to—they may need to see them. If the company makes a settlement offer and you’re satisfied, you’ll typically sign an acceptance, after which you'll receive payment or arrangements for repairs/replacement. If you’re not satisfied—for instance, if they deny a valid claim or offer a low amount—you have the right to dispute it.

Escalate if Needed (Arbitration or Complaints)

If you and the moving company can’t agree on a fair settlement, don’t lose hope. Interstate moving companies are required to participate in a dispute resolution (arbitration) program for exactly these situations. Essentially, arbitration is a neutral process where an independent arbitrator will review your claim and the mover’s response and decide the outcome. The mover must provide information on how to file for arbitration, which is usually included in your moving paperwork. If it's not, be sure to ask them. Arbitration can either be binding or non-binding depending on the program. However, in many consumer disputes, it’s typically binding for the mover—meaning if you win, they are required to pay. There is often a small fee to initiate arbitration, but it’s usually worth it if a lot of money is at stake. As another avenue, you can also file a complaint with the Federal Motor Carrier Safety Administration (FMCSA), especially if you suspect fraud or if the mover is not honoring their legal obligations. The FMCSA and state consumer protection agencies (like a state moving oversight office or the Attorney General) can apply pressure on a company to act in the customer's best interest. However, they usually don't get involved in resolving damage claims unless there’s a pattern of misconduct. Lastly, if all else fails, you can seek legal counsel—but this is rarely needed if you follow the steps above and use arbitration. Most reputable movers will settle legitimate claims without a legal battle.

Tips to Protect Your Belongings During a Move

While having insurance is essential, you also want to do everything possible to protect your belongings and avoid damage or loss in the first place. By being proactive and prepared, you can greatly reduce the likelihood of problems, and also ensure that if an issue does occur, your insurance coverage can fully help you. Here are some practical tips to safeguard your items and maximize your coverage protection.

Inventory & Photograph Your Items Before Moving

Create a detailed inventory list of all your major belongings and their condition before the move. For valuable or fragile items, take clear photos from multiple angles prior to packing. This serves two purposes—first, it helps confirm that everything leaving your old home arrives at the new one, and second, it provides proof of their original condition if you need to file a damage claim. If you have any items that are already a bit scratched or worn, you’ll know which damage was pre-existing (and so will the movers). For expensive items, note their serial numbers or any unique identifiers. Consider keeping a copy of this inventory in cloud storage or email it to yourself, so you can access it even if papers get lost in the shuffle.

Pack Carefully (or Let the Professionals Pack for You)

The way items are packed is crucial to their safety. If you’re doing your own packing, choose sturdy moving boxes and invest in quality packing materials—bubble wrap, packing paper, furniture pads, etc. Wrap fragile items generously and don’t leave empty space in boxes for things to shift. Label boxes containing breakables as “Fragile” so movers know to handle them carefully. Also mark boxes that should stay upright to prevent damage. If you’re unsure how to pack something delicate—like a large mirror or a chandelier—ask your mover for advice or let them handle those special items. Since damage to owner-packed boxes may not be covered unless there’s obvious mishandling, it might be worth paying the movers to pack high-value items professionally. Their packing not only provides better protection, but it also shifts responsibility to the mover for any internal damage. Don’t forget to secure things like dressers or appliances—remove loose items such as shelves, drawers, and knobs, and pack them separately so they don’t cause damage in transit.

Avoid Packing Certain Valuables & Essentials on the Moving Truck

As a rule, keep irreplaceable or extremely valuable items with you rather than on the moving van. This includes jewelry, personal electronics like laptops, important documents (e.g., passports, birth certificates, financial papers, etc.), family photographs and heirlooms, cash, and medications. Not only can heat, cold, or jostling in the truck potentially damage some of these items, but their loss would go beyond financial impact—and, as mentioned, movers often won’t cover these items fully. Pack a special box or bag that stays with you for these personal valuables. Additionally, carry an essentials bag with you that includes a change of clothes, basic toiletries, phone chargers, and any other necessary items so you’re not rifling through boxes looking for critical items on day one. By keeping your valuables and necessities in your own car or luggage, you reduce the risk of losing them and bypass any insurance coverage complications for those items.

Communicate Any High-Value or Unique Items

If you have any items that are unusually expensive—like original artwork, a high-end computer, grandfather clock, or vintage wine collection—tell your moving company in advance and in writing. This goes hand-in-hand with declaring items of extraordinary value for insurance purposes. Point these items out on moving day as well, so the crew knows to take extra care. Most movers appreciate knowing which pieces are most important to you. They might even crate or specially wrap certain items if needed. By being clear about what’s fragile or precious, you allow the movers to do their best job protecting those belongings. If you’ve purchased Full Value Protection, ensure those items are listed and covered to their full value, asking the moving company if any additional paperwork is needed. Communication is key to avoiding misunderstandings and ensuring adequate protection.

Label Boxes Clearly & Keep an Organized System

Proper labeling goes beyond just marking items as fragile. It’s wise to label each box with its general contents and the room it belongs to. This not only helps you during unpacking, but also helps movers know which boxes might contain breakables or heavy items. Use labels or marker on multiple sides of the box, so it’s visible no matter how it’s turned. Additionally, number your boxes and keep a checklist—e.g., 1 of 20, 2 of 20, etc.—so you can quickly verify that all boxes are accounted for when unloading. If any are missing, you’ll catch it immediately and can alert the driver. For disassembled items, put small parts such as screws or cables in labeled bags. Then, either tape them to the furniture they belong to, or keep a parts box to help prevent loss of these crucial pieces. An organized move is often a safer move because there’s less chaos and fewer things can slip through the cracks.

Choose a Reputable, Licensed Moving Company

Do your homework before hiring a mover. A reliable moving company with a track record of good service is far less likely to damage your items—and if they do, they’re more likely to honor your claim quickly. Make sure the mover is properly licensed and insured for your type of move (interstate movers should have a USDOT number and be registered with FMCSA, while intrastate movers should meet state regulations). Check reviews and ratings. An unlicensed mover might offer a low price, but they often provide little or no protection for your goods—and in worst-case scenarios, could even be running a moving scam. Protect yourself by choosing movers who are professional and trustworthy. Ask for recommendations, check for any complaints on file, and verify their insurance coverage. A great mover will also help you with all the tips above—they’ll guide you on packing, documentation, and more. Having a smooth move starts with hiring the right team.

Stay Involved on Moving Day

While you don’t need to micromanage the movers, it helps to be present and attentive during packing, loading, and unloading. If you see a box being placed upside down when it shouldn’t be, speak up. If a mover is stacking heavy items on top of fragile ones, intervene politely. Sometimes crews get tired or rushed, and a gentle reminder from you can prevent an accident. Also, do a final walkthrough of your old home before the truck leaves to ensure nothing was left behind—and don't forget to check the attic, basement, closets, and outdoor areas. At delivery, do the same in the truck’s cargo area, making sure everything has been unloaded. Being vigilant can prevent loss and give you a chance to catch any potential issues on the spot.

Understand Your Coverage & Follow Guidelines

Lastly, make sure you follow any requirements of your chosen insurance coverage. For example, if you opted for Full Value Protection, the mover might require you to report any obvious damage within a certain short time frame in addition to the formal claim later. If you purchased third-party insurance, know what their process is if you have damage, as you sometimes have to notify the insurer immediately, as well. Keep all paperwork—contracts, valuation addendums, and insurance policies—in a safe place so you can reference them. By understanding the rules of your coverage, you won’t accidentally void it or miss out on benefits.

***

Planning your next move? Our extensive moving resources—including guides, calculators, and more—can help you prepare! Plus, if you need temporary storage to help ease your transition, Extra Space Storage offers convenient facilities across the country. Find self storage near you!

Helpful Moving Tips & Tools

How to Set Up Utilities After Moving: Your Complete Guide

Moving to a new apartment or home soon? This guide takes you through how to set up utilities—including a step-by-step utility setup timeline.

Moving to a New Home? Use This 3-Month Moving Checklist

Moving to a new home? Whether it's to a new house or an apartment, moving can be difficult at times. Stay on track with our three-month moving to-do list!

Address Change Checklist: Who to Notify When You Move

Planning a move soon? Use this change of address checklist to notify the proper people and places that you're moving!

How Much Do Movers Cost?

Professional movers cost ~$550-$12,000. Learn the average cost of hiring a moving company for local and long-distance moves in this guide.

Best Tape for Moving Boxes

Planning a move? Buying the best packing tape for moving boxes is essential for a hassle-free move. Find out which tapes are best for moving boxes.

Author Profile

Quinn Johnson

Quinn Johnson is a moving expert and author for Extra Space Storage. He's moved over 15 times, including internationally, and helped countless others between their own homes. He's happy to lift some boxes for a friend as long as he's paid in pizza. As a writer and content creator for Extra Space Storage since 2019, Quinn shares helpful moving tips and info to alleviate the common stresses of moving.